The terms “term insurance” and “life insurance” are often used interchangeably in everyday conversation, but they are not the same thing. This confusion has led many Indians to buy insurance products that are either too expensive, provide inadequate coverage, or mix insurance with investment in ways that deliver poor results in both areas.

Understanding the difference between term insurance and life insurance in India is one of the most financially important pieces of knowledge you can have. This guide explains each type clearly, compares them honestly, and tells you which one makes sense for different situations.

What Is Life Insurance? (Broad Definition)

In broad terms, “life insurance” refers to any insurance product that provides a financial benefit to the policyholder’s family upon the insured person’s death. There are multiple types of life insurance, and this is where confusion begins.

The main categories of life insurance products in India:

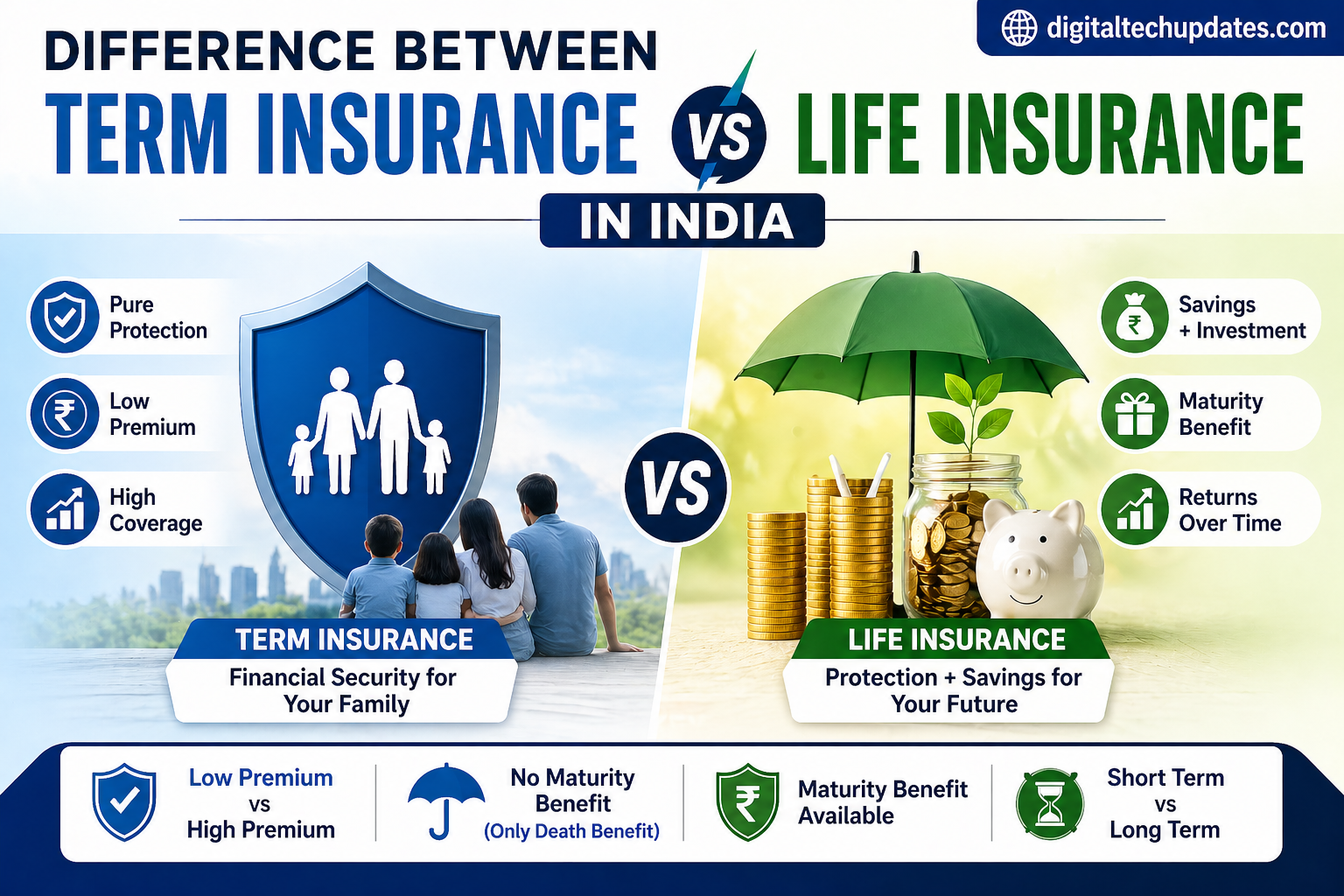

Term Insurance — Pure death benefit, no maturity benefit

Whole Life Insurance — Coverage for lifetime, with a maturity/surrender value

Endowment Plans — Combines insurance with a savings component

Money-Back Plans — Provides periodic payouts during the policy term

ULIPs — Market-linked investment combined with insurance

When people say “life insurance” in everyday conversation, they often mean endowment plans or money-back plans (the traditional LIC-type policies). When financial advisors say “life insurance,” they usually mean all of the above. This guide uses “traditional life insurance” to distinguish endowment and money-back plans from pure term plans.

What Is Term Insurance?

Term insurance is the simplest, purest form of life insurance. You pay a premium for a fixed period (the “term” — typically 20, 30, or 40 years). If you die during that term, your nominees receive the sum assured (the cover amount). If you survive the term, the policy expires with no payout and no return of premium (in the basic version).

Key characteristics of term insurance:

Very high coverage for very low premium: A ₹1 crore term cover for a healthy 30-year-old typically costs ₹8,000–₹12,000/year — less than ₹1,000/month

No investment component: Pure insurance only

No maturity benefit: If you outlive the policy, you receive nothing (and should consider this a good thing — it means you are alive)

Fixed duration: Typically chosen to cover working years until retirement

Return of Premium (ROP) variant: Some term plans offer “return of premium” — if you survive the term, your cumulative premiums are returned. This costs 60–100% more in premium and is generally not recommended by financial advisors, as the extra cost is better invested separately.

LIC AAO Apply 2025: Step-by-Step Guide to Online Application, Eligibility, Fees, Exam Pattern

What Are Traditional Life Insurance Plans?

Traditional life insurance (endowment plans, money-back plans, whole life plans) combines insurance with savings or investment.

Endowment Plan Example:

Premium: ₹50,000/year

Term: 20 years

Sum Assured: ₹10 lakh

If you die during the term: Family receives ₹10 lakh

If you survive: Receive ₹10 lakh + bonuses at maturity

Money-Back Plan:

Similar to endowment but pays out a percentage of sum assured every few years during the term

Remaining sum assured + bonuses paid at maturity or on death

Whole Life Plan:

Coverage for your entire lifetime (up to 99–100 years)

Builds surrender value over time

Premium paying term is typically 20–30 years; coverage continues for life

Key Differences: Term Insurance vs Traditional Life Insurance

| Feature | Term Insurance | Traditional Life Insurance |

| Primary purpose | Pure death protection | Insurance + savings |

| Premium cost | Very low (₹8,000–₹15,000/year for ₹1 crore cover) | High (₹30,000–₹80,000+ for same cover) |

| Sum Assured available | Very high (₹50 lakh–₹10 crore+) | Relatively low (₹5–₹25 lakh typically) |

| Maturity benefit | None (basic plan) | Yes — sum assured + bonuses |

| Investment returns | None — pure insurance | Low (5–6% typically, below FD rates) |

| Flexibility | Fixed term | Less flexible |

| Tax benefit | Yes (80C) | Yes (80C) |

| Recommended by experts | Yes, strongly | Generally no, for most people |

Why Most Financial Experts Recommend Term Insurance

The financial advice community in India — from chartered accountants to SEBI-registered investment advisors — almost universally recommends term insurance over traditional life insurance for most people. Here is why:

1. You can get dramatically higher coverage for a fraction of the cost.

A ₹50,000/year traditional endowment plan might give you ₹10 lakh of coverage. The same ₹50,000/year in term insurance gives you ₹1 crore or more of coverage. If the purpose of insurance is protecting your family financially in your absence, higher coverage is objectively better.

2. Traditional plans mix insurance and investment poorly.

The investment returns in traditional plans (typically 5–6% over 20+ years) are significantly lower than what a well-chosen mutual fund delivers (historically 10–12% for diversified equity funds in India). The insurance component is also inadequate for most families’ actual needs.

3. The “buy term and invest the rest” principle:

If you buy term insurance and separately invest the premium difference (between what traditional insurance would cost and what term costs) in mutual funds, you end up with far greater insurance coverage AND far greater investment wealth. This is the principle that drives the universal financial advisor recommendation.

Example:

Traditional LIC endowment: ₹50,000/year → ₹10 lakh cover + modest maturity

Term insurance: ₹10,000/year → ₹1 crore cover

Remaining ₹40,000/year invested in mutual fund SIP → ₹3–4 crore corpus over 25 years at 12% returns

When Does Traditional Life Insurance Make Sense?

Despite the generally unfavourable comparison, there are specific situations where traditional life insurance has merits:

Extremely risk-averse individuals: If you will not invest the difference and want guaranteed returns regardless of market performance, traditional plans provide certainty that term + mutual fund cannot.

Estate planning for high net worth individuals: Whole life plans can serve specific estate transfer and liquidity purposes for HNI families.

Forced savings for those without discipline: For people who genuinely will not invest separately, the forced savings element of traditional plans creates at least some corpus.

Specific riders and benefits: Some traditional plans offer guaranteed insurability and premium waiver benefits that may suit specific situations.

However, for the vast majority of Indian middle-class families, term insurance + mutual fund investments remains the superior strategy.

ULIP — A Third Category

ULIPs (Unit Linked Insurance Plans) are a hybrid product — part insurance, part market-linked investment. Premium is split between insurance coverage and an investment fund (similar to mutual funds).

Why ULIPs are generally not recommended:

High charges in early years (premium allocation charge, fund management charge, mortality charge) significantly reduce investment returns

Insurance coverage is typically inadequate relative to total premium paid

The same investment goals can be better achieved through mutual funds (lower cost, better regulated) + separate term insurance

Post-IRDA regulatory reforms have reduced ULIP charges, making modern ULIPs more competitive. However, the combination of higher complexity and mixed performance history means most financial advisors still prefer the simple term + mutual fund approach.

How to Choose the Right Sum Assured for Term Insurance

A common rule of thumb: your term insurance coverage should be at least 10–15 times your annual income.

More precise calculation:

Add up all outstanding debts (home loan, car loan, personal loans)

Add the income your family needs for the next 10–15 years

Subtract existing savings and investments your family could access

The result is your minimum coverage need

For a person earning ₹8 lakh/year with ₹30 lakh in home loan and ₹10 lakh savings, a rough calculation:

Income replacement for 15 years: ₹1.2 crore

Outstanding debt: ₹30 lakh

Less existing savings: -₹10 lakh

Coverage needed: ~₹1.4 crore → round up to ₹1.5 crore cover

Best Term Insurance Providers in India 2026

| Company | Claim Settlement Ratio (2024–25) | Notable Strength |

| LIC (e-Term) | 99%+ | Government backing, highest trust |

| HDFC Life Click2Protect | 99.2% | Private sector leader, strong brand |

| ICICI Prudential iProtect Smart | 97.9% | Flexible options, good digital experience |

| Max Life Smart Term Plan | 99.2% | Excellent claim settlement record |

| Tata AIA Sampoorna Raksha | 98.9% | Competitive pricing |

| SBI Life eShield | 96.7% | Good for SBI bank customers |

Claim Settlement Ratio (CSR) is the most important metric — it shows the percentage of claims the company has settled. Always choose a company with 97%+ CSR.

FAQs

Q1. Is LIC term insurance better than private insurance companies?

LIC has government backing (implicit guarantee), making it extremely trustworthy. However, private companies like HDFC Life and Max Life have very high claim settlement ratios and often offer more features at competitive prices. Both are excellent choices.

Q2. At what age should I buy term insurance?

The younger you buy, the lower your premium. The ideal time is your late 20s or early 30s, once you have financial dependents. Buying at 28 rather than 38 can save ₹5,000–₹8,000 per year in premium for the same cover.

Q3. How long should my term insurance policy be?

The policy should cover you until your financial dependents are self-sufficient and your retirement corpus is built. Typically, this means covering until age 60–65. A 30-year-old should look at a 30–35 year term.

Q4. Can I have both term insurance and traditional life insurance?

Yes. Some people keep existing traditional plans (especially those paid over many years) for the guaranteed corpus while buying term insurance for the actual death benefit coverage needs.

Conclusion

The difference between term insurance and traditional life insurance in India comes down to this: term insurance provides maximum financial protection for your family at minimum cost, while traditional life insurance combines insurance with low-return savings in a way that serves neither purpose optimally.

For most Indians — young earners, salaried employees, small business owners — the clear recommendation is term insurance for protection and separate mutual fund SIPs for investment. This combination delivers more coverage and more wealth than any traditional insurance plan.

Buy term insurance early, keep the premium low relative to your income, and invest the difference wisely. That is the foundation of sound financial protection.

For more finance guides, visit DigitalTechUpdates.com.