Walk into any major electronics store in India or browse through Amazon or Flipkart, and you will see smartphones advertised with “No-Cost EMI” prominently displayed. The proposition seems irresistible — buy a ₹50,000 phone and pay just ₹4,167/month for 12 months with “zero interest.” But is no-cost EMI truly cost-free? And is it the right choice for your next smartphone purchase?

This article breaks down exactly what no-cost EMI is, who actually bears the cost if interest is zero, the genuine benefits it offers, the hidden disadvantages many buyers miss, and how to decide whether it makes sense for you.

What Exactly Is No-Cost EMI?

No-cost EMI (also called zero-cost EMI or 0% EMI) is a financing scheme where a buyer can purchase a product and pay in monthly instalments with no interest charged on the principal amount.

A standard EMI for a ₹48,000 phone at 14% annual interest for 12 months would cost approximately ₹4,323/month, with ₹3,876 paid as interest over the year. With no-cost EMI, you pay exactly ₹4,000/month for 12 months — ₹48,000 total.

At face value, this looks genuinely cost-free. The complexity lies in how the “no interest” part is actually structured.

How No-Cost EMI Actually Works (The Hidden Part)

The interest is not eliminated — it is redistributed. Here is how:

Method 1 — Discount removal: The product is listed at a discounted price (e.g., ₹45,000 after ₹3,000 bank discount). However, when you choose no-cost EMI, the discount is removed and you pay ₹48,000. The ₹3,000 discount effectively “pays” the processing fee or interest cost. You never receive the discount.

Method 2 — Upfront processing fee: The bank charges a processing fee (typically 1–3% of the loan amount) which is collected upfront. This is essentially the interest cost in a different form.

Method 3 — Manufacturer/retailer subsidises the interest: In some genuine no-cost EMI schemes (particularly direct brand offerings), the brand or retailer pays the interest to the bank as part of their promotional cost. This is relatively rare and is the only truly cost-free version.

Method 4 — Cashback structure: Some platforms offer no-cost EMI where the interest is offset by a cashback credited to your account. Read the terms carefully — cashback may be restricted to platform wallet credits rather than direct refund.

In summary: “No-cost” almost always means the cost is shifted or hidden rather than eliminated. Knowing this helps you make an informed decision.

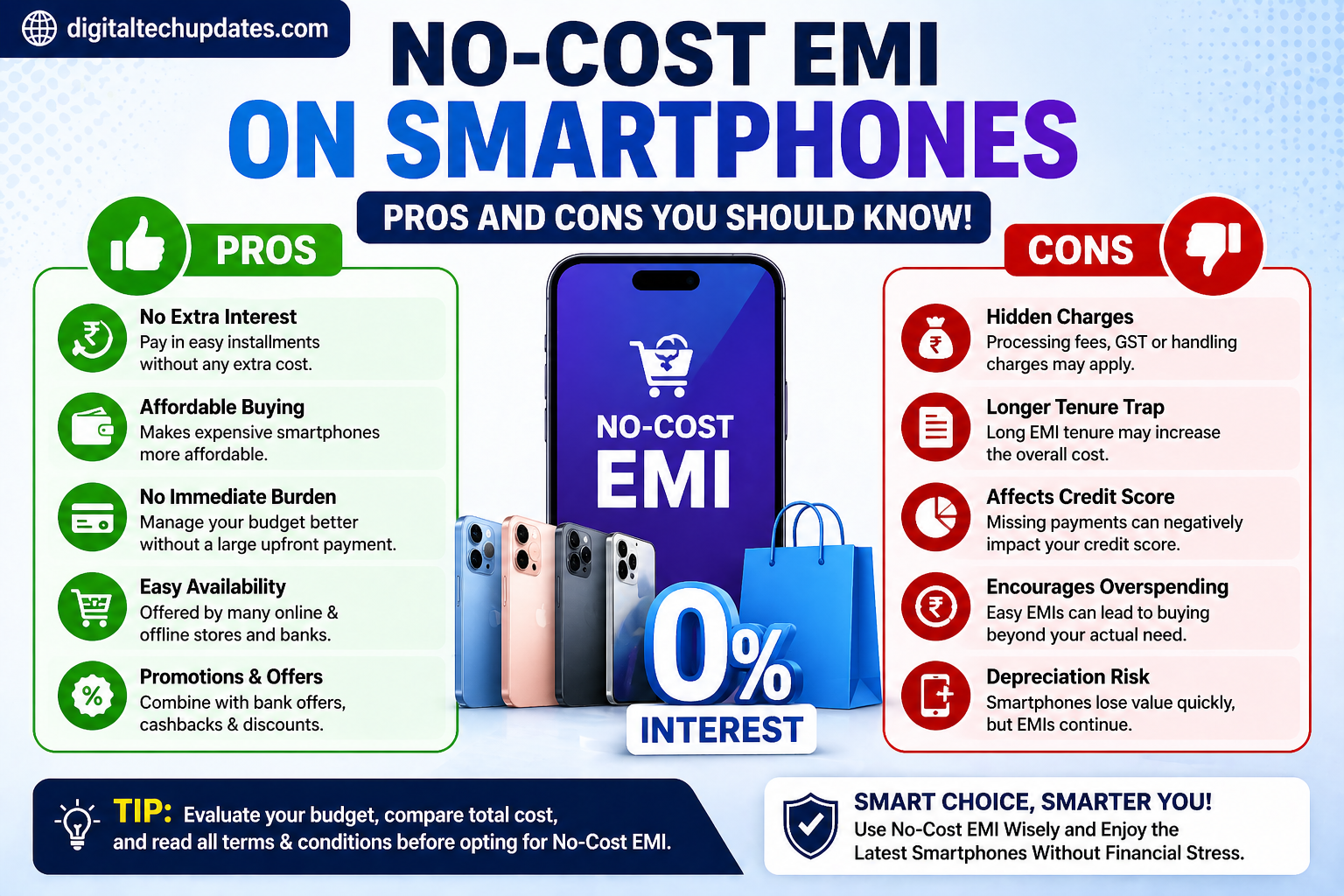

Pros of No-Cost EMI for Smartphones

Despite the cost structure complexity, no-cost EMI offers real, legitimate benefits:

Preserves cash flow: Instead of paying ₹50,000 upfront, you spread the payment over 6–12 months. Your savings or investments are not disrupted.

No opportunity cost if invested: If you have ₹50,000 in liquid savings earning returns, keeping that money invested while paying EMIs means your money keeps working for you.

Genuine benefit for true interest-free schemes: When a brand genuinely subsidises the interest, you truly pay nothing extra for the convenience.

Accessible flagship smartphones: No-cost EMI makes premium smartphones accessible to buyers who could afford the monthly payment but not the full upfront cost.

Credit card reward points: When you pay via credit card EMIs, you often earn full reward points or cashback on the entire purchase amount upfront.

Cons and Hidden Costs of No-Cost EMI

1. You likely lose the discount: The most common no-cost EMI mechanism removes your eligibility for bank discounts, cashback offers, or sale prices.

2. Processing fees: Many schemes include a processing fee of 1–3%. On a ₹50,000 phone, that is ₹500–₹1,500.

3. Impact on credit card limit: The full purchase amount is blocked from your credit limit for the EMI duration.

4. GST on interest waiver: Under Indian tax rules, the GST on the interest component that is waived is sometimes passed to the customer.

5. Over-buying temptation: The low apparent monthly cost can tempt buyers to purchase more expensive phones than they would otherwise consider.

6. Credit score implications: Multiple active EMIs can affect your credit utilisation and, in extreme cases, impact loan eligibility for important purchases.

No-Cost EMI vs Regular EMI

| Factor | No-Cost EMI | Regular EMI |

| Interest charged | None (or hidden in pricing) | Explicit interest at 12–24% |

| Processing fee | Often applicable | Often applicable |

| Discount eligibility | Usually lost | Usually retained |

| Transparency | Less transparent | Fully transparent |

| True cost | Depends on discount scenario | Clear from EMI schedule |

When No-Cost EMI Makes Sense

You have a stable monthly income that comfortably covers the EMI without stress.

The product is not on sale and no bank discount applies — meaning you are not giving up anything.

You would otherwise disrupt investments or savings to make the purchase.

The brand is subsidising the interest (genuine during festive season launches).

You earn credit card rewards that add value beyond the EMI convenience.

When You Should Avoid No-Cost EMI

You are losing a significant discount by choosing EMI over a direct bank offer.

You already have multiple active EMIs — additional burden increases financial stress.

You are buying above your actual budget — if you cannot afford the monthly cost, the EMI is masking an unaffordable purchase.

Short tenure EMI for small amounts — the processing fee makes it barely worthwhile.

You are not a credit card holder and use a consumer finance company with high default penalty clauses.

Tips Before Choosing No-Cost EMI

Always compare the effective price: Find the lowest available price on the phone via any method. Then compare what you would pay on no-cost EMI.

Read processing fee terms: The checkout should clearly state any processing fees.

Check your credit card terms: Understand how EMI affects your credit limit and GST charges.

Use the EMI calculator: Compare 6-month and 12-month tenure options.

Check cashback terms: Confirm whether cashback is credited to your bank account or as platform wallet credit.

FAQs

Q1. Is no-cost EMI truly free?

Rarely in the purest sense. Most schemes either remove your discount eligibility, charge processing fees, or recover the interest cost through GST on the waived amount.

Q2. Which cards offer the best no-cost EMI on smartphones in India?

HDFC Bank, SBI Card, Axis Bank, ICICI Bank, and Kotak credit cards offer no-cost EMI on most major platforms. HDFC and SBI Cards have the widest acceptance.

Q3. Does no-cost EMI affect my credit score?

Yes, in the sense that your credit utilisation increases. Multiple simultaneous high-value EMIs can reduce your score.

Q4. Can I foreclose a no-cost EMI early?

Yes, but some banks charge a foreclosure fee (typically 2–3% of outstanding principal).

Q5. Is buying a phone on no-cost EMI better than saving up and buying?

Financially, saving and buying upfront is marginally better. However, if the phone serves a genuine professional purpose, the cash flow convenience often justifies it.

Conclusion

No-cost EMI on smartphones is a genuinely useful financial tool when used wisely. The key is understanding what you may be giving up, what fees may apply, and whether your monthly budget absorbs the EMI comfortably.

For more technology and finance guides, visit DigitalTechUpdates.com.